Good Debt Pays for Itself, Bad Debt is a Drag…

Top 3 Takeaways:

- How to identify good debt and bad debt

- To consider the history of government debt & why it matters

- The multiple effects of bad spending decisions

I thought we’d muse today on how presidential leadership and economic policy impact government budgets and deficits and ultimately, how our perspective on debt affects us as individuals, businesses, and the nation.

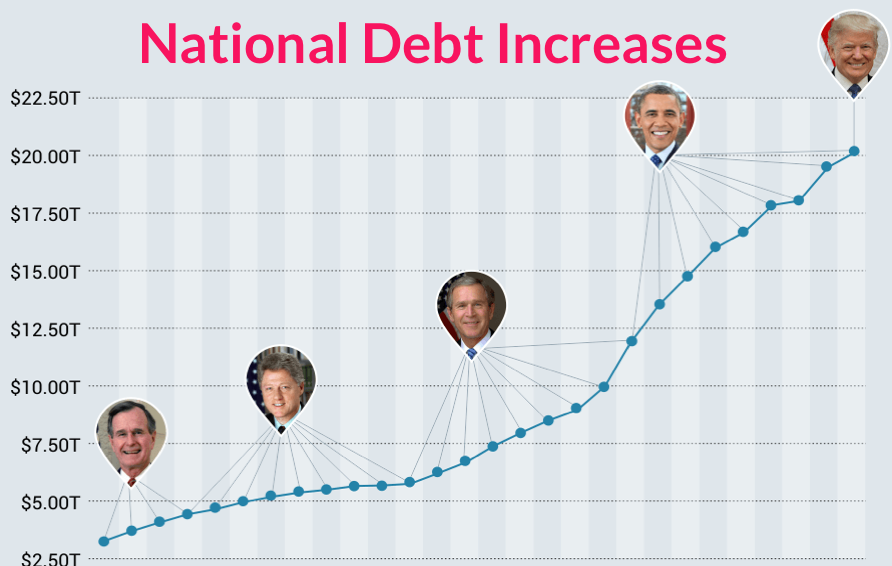

Donald Trump has been a remarkable President, in many ways, but I’ll limit myself to one area of focus today. With a Presidency predicted by the Simpsons 16 years before Trump first took office, our national debt has grown at a ferocious pace, up to a new record for the good old US of A at 136% of GDP. Of course, we just added a fresh $3T or so, to a whopping $26.5T. (The T stands for Trillion, if you’ve been living under a rock).

Prior to this point, Trump was doing pretty good, going up from 104% of GDP when he started to 106% by 2019, despite tagging on an additional $3T onto the sum during his first three years - GDP was growing quickly also, making the ratio relatively stable. Obama before him had grown the debt from $10T to $16T in his first term (68% up to 99% of GDP) and up to $19.5T and 104% of GDP during his second term. Of course, Obama first took the office right on the front end of The Great Recession - if debt goes up and the economy shrinks, the ratio swings quickly - as in 2020. This tops the previous record set in the aftermath of WWII, when it was up to 119% during Truman’s first term in office.

This ratio got down into the low 30%’s for periods of the 60’s and 70’s, before the Reagan tax cuts sent it back up toward 50%, and then held pretty stable through the Clinton years (we even had a surplus 1 year!), before the Iraq war started our current and largely unbroken upward trend. In the past, our society has deemed that 100% level as fairly dangerous it seems, and worked to pay it off when it got too high. I looked at a few sites, and took my data from this table here.

Thinking about debt is an exercise best done with ratios and percentages, and philosophy, I would argue. It’s something I know a fair bit about, having been a small business lender for just shy of 15 years (it’s 14 years 10 months, but I usually just say 15 - is that ok?). In addition, I’ve generally suffered* from I-Want-It-Now Syndrome for most of my life, and exited college with both credit card balances and student loans (*but I had a lot of fun and didn’t work too hard during school).

I married the amazing Jill Bear in my late 20’s, and our household, and especially my income grew steadily throughout my banking career, and my ratio was it’s best ever toward the end of it, enough that we could qualify to purchase our current home without having proved rental income on our prior - which became a rental property for us. With positive cash flow from our rental property, and an income still on the upswing, we had beach vacations and cruises, and went to a lot of restaurants and music festivals and whatnot. Discretionary cash flow is fun!

But then I quit my bank job, and tried to start a restaurant but wound up with a food trailer - Bear’s Backyard Grill - do you remember it?! My income went from the high 5-figures to the barely 5-figures overnight, which was nearly as much as Jill’s income at the time. What had been a comfortable mortgage payment and a small credit card obligation became difficult to service, and discretionary spending had to be eliminated almost completely. We were in negative cash flow mode for a couple of years there - being in the food business we always ate ok - lots of leftovers, and we always had cash but we never had any money. We were forced to sell the rental property eventually to keep the dream alive, but then realized the dream was more likely to become a nightmare. Besides, I’d found a new love in LoCo Think Tank so we sold the food business and I got a job and we began a slow progression back into the lower middle class. Jill got a big promotion that nearly doubled her income along the way (and gave her a very fulfilling role), and I’ve been able to steadily grow LoCo and my income thereof (though it’s still far below banker income). Once again have a bit of discretionary spending for restaurants, and maybe even a music festival next year if such things are allowed again.

I don’t say all this as a confession, although I suppose that it is, but to personalize it and allow you to understand the feels involved with paying debt, and especially how it’s related to the income generated. At best, it’s annoying, and when things are really tough, it downright hurts. That rental would be worth another $150K today, with great cashflow! I was a small business lender for (*almost) 15 years, and I believe in financing and using leverage to help a business (or even a person or a nation) grow, and so I want to contrast for and with you the difference between Good Debt and Bad Debt.

Good Debt pays for itself. Bad Debt is a drag.

Good debt might be used for the acquisition of a piece of equipment that can increase productivity. More widgets in less time = more profit, some of which can be diverted to pay back the debt. Good debt might be used to acquire education or skills, which increase earning potential, some of which can be used to pay back the debt. Good debt might be used to purchase a home, to allow a person or family to build equity and live in a stable environment rather than renting from various landlords for various periods of time. Good debt might be used to acquire rental properties, with tenant payments paying the mortgages and building additional equity for the owner over time. Good debt might even be used to purchase a reasonable automobile, the alternative being a pain-in-the-A bus route or dependency on Uber or Lyft.

Bad debt might be used to purchase a luxury sports car, which will rapidly depreciate and the servicing of which will be a discretionary cash flow drag. Bad debt might be purchasing an unnecessary piece of equipment in a business, that will see only limited use on work that could easily be outsourced. Bad debt might be used to help a real estate speculator acquire excessively leveraged properties that may tip into foreclosure and threaten neighboring property values and the financial security of the speculator. Bad debt might fund the operating losses of a small business, allowing them to put off addressing the core issues affecting their profitability. And, bad debt may be held by the banks that issue it - just one loan being not repaid can impact a bank’s bottom line dramatically, and when lots of loans go bad banks don’t have any money to loan to businesses that can actually pay it back.

So, let us macro this up a bit, huh? We’re facing an election this fall, where Trump may be granted the opportunity to continue (or reverse) his remarkable legacy of Debt/GDP ratio growth, or where Biden will take his turn at the wheel. He’s no Lisa Simpson though (bummer, amiright?), and regardless of the outcome I would say it’s a good time for our citizenry to be actively involved in a discussion of how Uncle Sam spends our tax dollars, and how much deeper we allow him to go into the hole.

Good spending might be the global effort to defeat the Nazi’s in WWII. Or it might be on repairing or building new infrastructure, concrete and fiber, allowing for a more efficient economy. It might be spent on job training programs or innovative rural and inner city economic development initiatives. It might even be extended unemployment benefits to prevent suffering and further economic damage caused by the response to the pandemic threat.

But there is bad spending too. The $600 extra unemployment benefit, that caused too many of my business owner members to have to make new hires because some of their people could make more money by staying home - bad spending. Programs that build sustained dependency on government rather than activating a path to self-sufficiency - bad spending. Transfer programs that suck 70 cents out of every dollar for administrative requirements - bad spending. Dropping bombs on infrastructure and people in an attempt to push governments out of office, to “free” a people we don’t care about, and developing new America-haters with every bomb - bad spending.

Sometimes it’s hard to judge the difference between good and bad in this world, and sometimes it’s pretty easy. With debt (and spending & investment), I think it’s fairly simple - good debt pays for itself! Sometimes we need the benefit of the rear-view mirror to truly determine, but we can use history and intuition (and especially, common sense) as our guide. Paying down our national debt is going to hurt, over an extended period of time, and the bigger it gets the more it will hurt. And if we’re going to deficit spend in coming years (as it appears we almost certainly will), let’s at least make sure it’s the kind of spending that pays for itself. And, bring this same principal into your homes and your businesses, too - because bad debt (and bad spending) is a drag.